Bitcoin$11,463.550.21%

Bitcoin$11,463.550.21% Ethereum$375.130.45%

Ethereum$375.130.45% Bitcoin Cash$246.80-0.86%

Bitcoin Cash$246.80-0.86% XRP$0.241101-0.58%

XRP$0.241101-0.58% Litecoin$47.09-1.01%

Litecoin$47.09-1.01% Cardano$0.1066260.55%

Cardano$0.1066260.55% IOTA$0.269023-1.52%

IOTA$0.269023-1.52% Dash$66.62-0.65%

Dash$66.62-0.65% NEM$0.110292-3.87%

NEM$0.110292-3.87% Monero$123.770.90%

Monero$123.770.90% Stellar$0.0825761.91%

Stellar$0.0825761.91% EOS$2.540.42%

EOS$2.540.42% Ethereum Classic$5.20-0.65%

Ethereum Classic$5.20-0.65% Lisk$1.101.95%

Lisk$1.101.95% TRON$0.025796-0.52%

TRON$0.025796-0.52% NEO$17.25-2.05%

NEO$17.25-2.05% VeChain$0.011430-1.67%

VeChain$0.011430-1.67% Qtum$2.18-1.45%

Qtum$2.18-1.45%

Bitcoin Gold$7.70-0.41%

Bitcoin Gold$7.70-0.41% OMG Network$3.30-1.60%

OMG Network$3.30-1.60% ICON$0.372259-2.88%

ICON$0.372259-2.88% Nano$0.820.54%

Nano$0.820.54% Verge$0.004353-0.93%

Verge$0.004353-0.93% Zcash$62.71-0.70%

Zcash$62.71-0.70% Ontology$0.55-2.10%

Ontology$0.55-2.10% Aeternity$0.106353-0.76%

Aeternity$0.106353-0.76% Steem$0.155436-1.27%

Steem$0.155436-1.27% Wanchain$0.258405-1.86%

Wanchain$0.258405-1.86% Siacoin$0.002880-0.36%

Siacoin$0.002880-0.36% BitShares$0.018660-0.75%

BitShares$0.018660-0.75%

Bytom$0.061324-0.43%

Bytom$0.061324-0.43% Zilliqa$0.017932-2.32%

Zilliqa$0.017932-2.32% Populous$0.3613023.56%

Populous$0.3613023.56% Bitcoin Diamond$0.51-2.02%

Bitcoin Diamond$0.51-2.02% Stratis$0.409018-2.35%

Stratis$0.409018-2.35% Waves$2.98-7.88%

Waves$2.98-7.88% Maker$570.292.03%

Maker$570.292.03% Dogecoin$0.0025970.33%

Dogecoin$0.0025970.33% HyperCash$1.05-1.66%

HyperCash$1.05-1.66% Status$0.023314-1.53%

Status$0.023314-1.53% DigixDAO$47.211.15%

DigixDAO$47.211.15%

The Future of Fintech in Southeast Asia – Finch Capital & MDI Ventures

According to a recent fintech report from Finch Capital and MDI Ventures, the current pandemic is leading to increased access to (and need for) digital banking services.

As many as 50% of SEA consumers are unbanked; 70% are either underbanked or unbanked. Today, cash is still the primary means of transactions. 70% of SME merchants accept only cash in 2019.

The Covid-19 outbreak has drastically accelerated SEA’s shift to a cashless world, with unprecedented growth in the number of e-payment transactions amid a sharp decrease in cash withdrawals and deposits.

Banking, digital payments and loan-financing services greatly propelled the economic wheel forward throughout the lock-down. Since many fintech firms are startups, their agility to pivot their operations to provide specialized services as customers needed them strengthened the industry.

Indonesia, Singapore and Vietnam are the most attractive immediate opportunities. Indonesia’s internet economy has more than quadrupled to more than $40 billion in 2019 and is well on track to reach $130 billion by 2025.

The runner up is Vietnam with $12 billion in 2019 with a projected $43 billion by 2025. The biggest contributors are the e-Commerce and Ride-Hailing sectors.

Particularly in Vietnam, homegrown marketplaces like Sendo and Tik, who compete with the likes of Lazada and Shopee, are their key economic drivers.

Singapore continues to dominate funding and is the #1 regional base for fintech firms with $2.6B raised since 2015, led by big gains in funding to payments and insurtech startups.

E-money transaction in Indonesia skyrocketed 173% from January 2019 to January 2020, and the two key players were Gojek and OVO. Gen Y and Gen Z are fueling the rapid growth of e-payments and peer to peer lending.

Alternative lending startups in Indonesia attract the most funding and secure the highest number of deals of any fintech segments. A young population is driving adoption, being more open to alternative lending investments compared to the traditional institutional lending.

In Singapore,the future will be powered by AI and Blockchain. Since 2016, artificial intelligence and blockchain enabled fintechs in Singapore have gained significant traction.

The limited number of such fintech startups make them even more attractive to investors. In May, the Monetary Authority of Singapore kicked off efforts to develop a framework to ensure the “responsible” adoption of artificial intelligence (AI) and data analytics in credit risk scoring.

While In Vietnam, cash is king. A huge digital payments opportunity is rapidly evolving. 90% of Vietnamese consumers opt to pay cash on delivery for their online purchases, a much higher proportion than other regional markets.

However, digital payments technology is evolving rapidly. Payments through mobile banking services surged by a whopping 144% per year over the past five years.

The rise of digital payments in Vietnam is supported by the Government. To date, 33 payment licences have been issued by the State Bank of Vietnam, at a rate of around 1 licence every two months.

When it comes to SEA’s digital banking race, banks like DBS and UOB in Singapore, CIMB in Malaysia, Vietnam Prosperity JSCB and PT Bank BTPN TBK in Indonesia are leading the way.

At least seven digital-only banks owned by large traditional financial institutions operate in Indonesia, the Philippines, Thailand and Vietnam. Central banks in Singapore and Malaysia are preparing to open the banking industry to digital players.

Regulators in the Philippines and Thailand have expressed interest in developing virtual banking frameworks, and other countries could follow suit. Although the onset of virtual banking regimes will bring in more competition, large incumbents are already learning the tricks of the trade with their digital-only banks.

The future is to enable these incumbents with software. The next step is to enable these incumbents with software. In late June 2019, the Monetary Authority of Singapore (MAS) announced its intention to issue five digital bank licenses to eligible applicants.

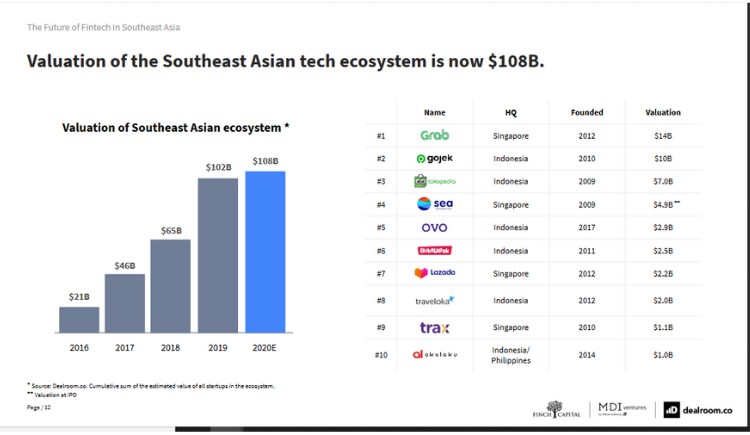

Fintech is Southeast Asia’s largest venture capital investment category by number of backed startups. The rise of fintech is accelerated by venture capital investment.

Last year, $1.6B was invested in the region, compared with only $0.2B five years ago. Much of the increased investment in SEA fintech startups is driven by foreign investment.

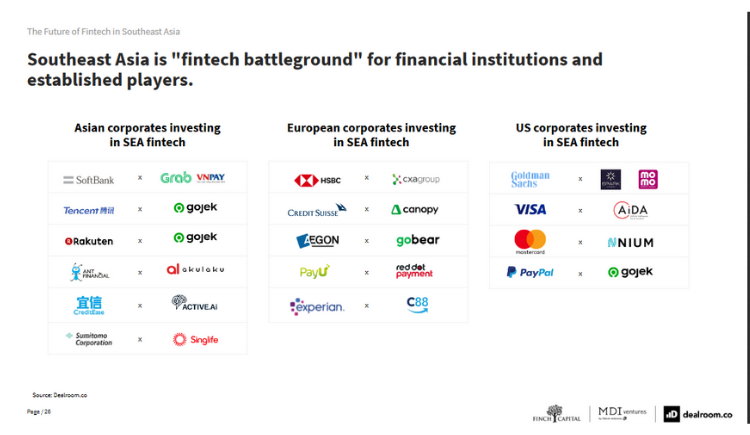

Through collaborations, fintech companies and Banks can have access to broader markets, along with a number of other benefits such as a faster route to product-market fit where fintech companies can attain early adopters from Banking clients.

The report highlights that collaborating instead of competing with fintechs can provide innovative tech-solutions for Banks.

For example, shared services and knowledge will improve product offerings through data analytics tools like predictive analytics, offering deeper engagements with customers.

The report concludes that the shift from disruption to collaboration is largely driven by the use of a more collaborative business model such as B2B2C.

Finch Capital’s investment thesis in Southeast Asia.

●Stage: Seed – Series A (Early Stage)

●Themes: Fintech in Southeast Asia are still in its early-days, with current startups concentration still around traditional fintech applications e.g. Payment & Lending. Wealth Management, Insurance Technology, and Property Technology are predicted to be the next wave along with the applications of fintech in non-financial sector or Embedded Fintech.

●Market: Indonesia is already Southeast Asia’s largest economy but it is now also poised to become the region’s largest Fintech hub by 2025 at an estimated USD 130 Bn. The large number of unbanked and underbanked population make it ripe for digital penetration.

●Business Model: Successful shift from disruption to collaboration between fintechs & financial institutions are largely driven by the use of complementary business model (B2B2C); enabling faster product market-fit and scalability across multiple channels.

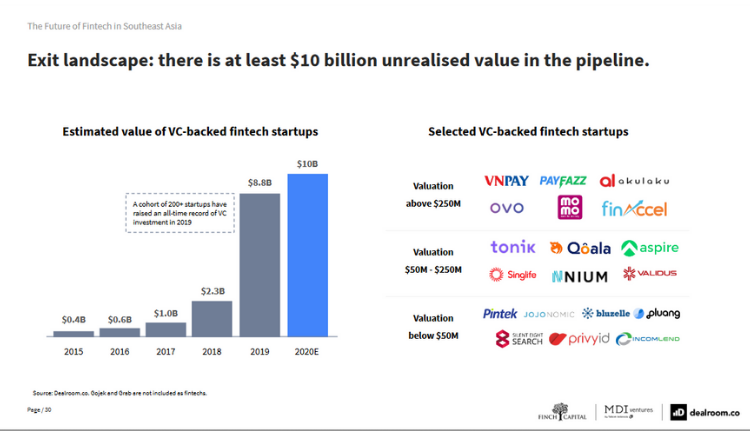

●Exits: We expect 100+ Fintech exits in the region between 2020-2023 to be driven largely by consolidation play around the Payment space and later Wealth Management – where we see local tech companies as the main acquirers.

Source: FINCH CAPITAL, MDI VENTURES and Dealroom.co

Follow Asia Blockchain Review on:

- Telegram: https://t.me/asiablockchainreview

- Facebook: https://www.facebook.com/pg/asiablockchainreview

- Twitter: https://twitter.com/abr_blockchain

- LinkedIn: https://www.linkedin.com/company/asia-blockchain-review/

- Website: https://www.asiablockchainreview.com/

- Email: [email protected]

- Youtube: https://www.youtube.com/channel/UCMQ5CVu0c9-pMlwB8LUvkiA

Related Article

November 21, 2020

November 20, 2020

November 20, 2020

November 19, 2020

We provide information about Asia Blockchain Review latest activities as well as global blockchain news and research. Subscribe to our Newsletter now or Contact us